The Explosion Heard Around the (College Basketball) World

- Scott Kaplan

- Feb 26, 2019

- 8 min read

Updated: Apr 3, 2019

(This post is co-authored with Sofia Villas-Boas)

Last Wednesday, with the NBA on its post-all star break, the world was focused on the most heated and historic rivalry in college basketball: Duke vs. North Carolina. Ticket prices were historically high (even approaching Super Bowl prices!!), and it’s no secret that Zion Williamson (widely considered the most exciting NBA prospect since LeBron James) had something to do with it. The superstar effect in basketball is real – if you’re a basketball fan there’s no doubt a big part of the reason you go to a game or watch on TV is to witness players like LeBron James make championship-clinching blocks (sorry Warriors fans) or Stephen Curry make ridiculous three-pointers (Head Coach Steve Kerr’s reaction might be even better). Some of my current research focuses on this exact effect – as you might imagine, there are significant price drops when superstar players are announced as “out” for games, and significant welfare losses to fans when they don’t get to watch them play. Our paper (which you can access here, if you’re interested) uses 2017-18 secondary ticket marketplace data to assess price changes when NBA superstars are announced to be out of games. We find that for popular players like Steph Curry, Anthony Davis, and Kyrie Irving (LeBron played every game last season), there are economically meaningful impacts ranging from a 7-25% ($9-$25) reduction in the average ticket price for matchups in which they are absent.

Back to college basketball’s biggest superstar, Zion Williamson. Less than a minute in to the UNC vs. Duke game, something truly crazy happened: Zion Williamson planted his left foot and COMPLETELY broke through his own shoe (the Paul George 2.5 shoe, in case you’re a sneakerhead like PJ Tucker). Yes, that’s not an exaggeration – check out the video and photo evidence:

Source: ESPN

For basketball fans, your first hope is that he’s not seriously injured (which it doesn’t appear that he is). This guy is a generational talent, set to make tons of money and support his family for years to come (at least he has an insurance policy). This event only served to reignite the dialogue about NCAA/NBA rules about kids going straight to the NBA out of high school (afterwards, the NBA actually proposed to reduce the required age to enter the draft from 19 to 18).

While that dialogue will undoubtedly continue, the economist in me was interested in something different – what would be the fallout for Nike? This reminded me of Nike’s announcement in early September that Colin Kaepernick would star in their “Just Do It” campaign. Everyone from sports media to other news sources to (unsurprisingly) our president got in on this – saying that this was a terrible move for Nike, pointing to the ~3.2% decrease in their stock price that day.

Hoooold up; let’s not attribute causality so fast. Did anyone bother to take a look at other notable sports shoe/clothing company stock prices? AKA, look at trends of “counterfactual” companies? I know my guy Max Kellerman (co-host of First Take on ESPN) did – he’s one of my favorite sports personalities because he actually understands statistics. What happened to Adidas? Oh yeah, they also dropped…actually by a very similar amount (look at the dip between August 31st close and September 4th open). Looks like this might not have been a bad day for Nike because of Colin Kaepernick, maybe just a bad day for sports shoe/apparel companies (or potentially an even broader set of companies).

Okay, so I was annoyed for a bit, but soon let it go. Then Zion’s shoe explosion happened. I remembered how the commentary would probably go once again – let’s just look at Nike’s stock price and see if it fell. The next day I ran into Sofia, a fellow econometrician and avid college basketball fan who also looks forward to the best time of the year in sports ("March Madness" of course). I told her that “Nike was down today,” and in brilliant Sofia fashion I received an email later that night with a complete set of lecture notes and code saying that she’s going to use this as a case study for her undergraduate econometrics class next week. This time, we economists needed to stand up for the sake of counterfactuals and correct, causal inference-based statistics. Did Zion’s shoe explosion actually have a causal impact on Nike’s stock price? The basketball econometricians wanted to find out.

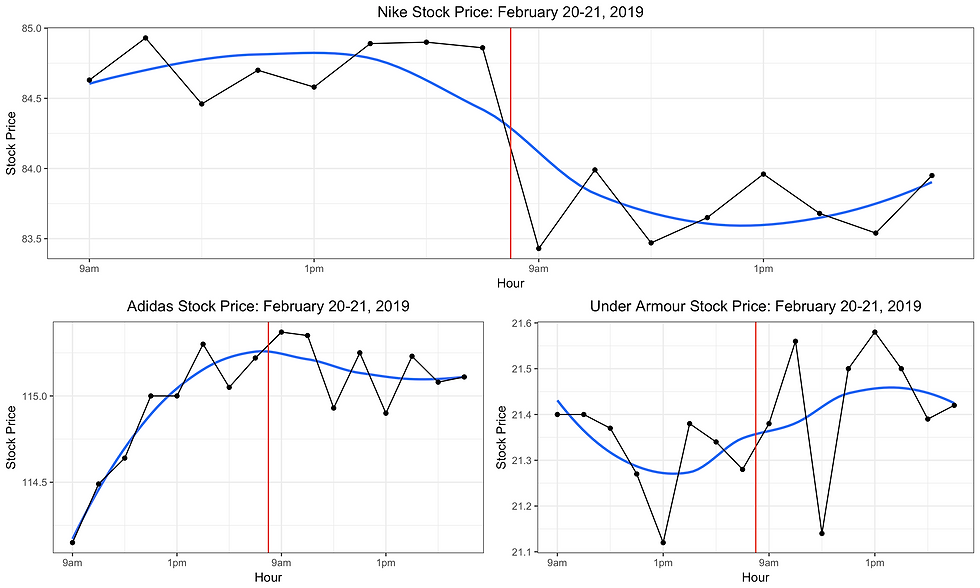

Let’s take a look at a graph of hourly stock prices for Nike, Adidas, and Under Armour on February 20th and 21st (16 hours of stock price data for each company). Adidas and Under Armour are widely known as the second and third most popular basketball shoe brands, respectively (we see you though, Puma). Zion’s explosion came after the stock market closed on the 20th, but before it opened on the 21st, and so the red vertical line indicates the timing of the explosion relative to the stock market’s open hours.

Looks like there was a big dip in Nike between closing bell on February 20th and opening bell on February 21st. Additionally, it doesn’t look like much happens to Under Armour and Adidas in response to the explosion (Under Armour goes up upon opening on the 21st, but then falls quickly after, giving a relatively flat trend over the course of February 21st).

So, are we done? Looks like we can just use Nike’s fall as the causal effect, right? Nope, there is one other primary concern in this setting to worry about – we need to make sure that the stock prices of Nike and the counterfactual group (Adidas and Under Armour) were trending the same direction before the explosion. Why do we need to do this? Without going too far down a proverbial econometric rabbit hole, this basically convinces us that these stocks would have moved in the same direction without the explosion. If the stocks are trending differently before the explosion, it’s harder to gauge the true impact on Nike’s stock price compared to Adidas’ and Under Armour’s prices, because there may have been other factors causing the trends to be different. In other words, the pre/post comparison we need between these two groups isn’t reliable. To be clear, we are still making a very important assumption that there is not another event that happens at the same time of the explosion that may have affected either the counterfactual group or Nike differentially. Given the magnitude of this shock and its exogenous (random) nature, I feel pretty good that this assumption is satisfied.

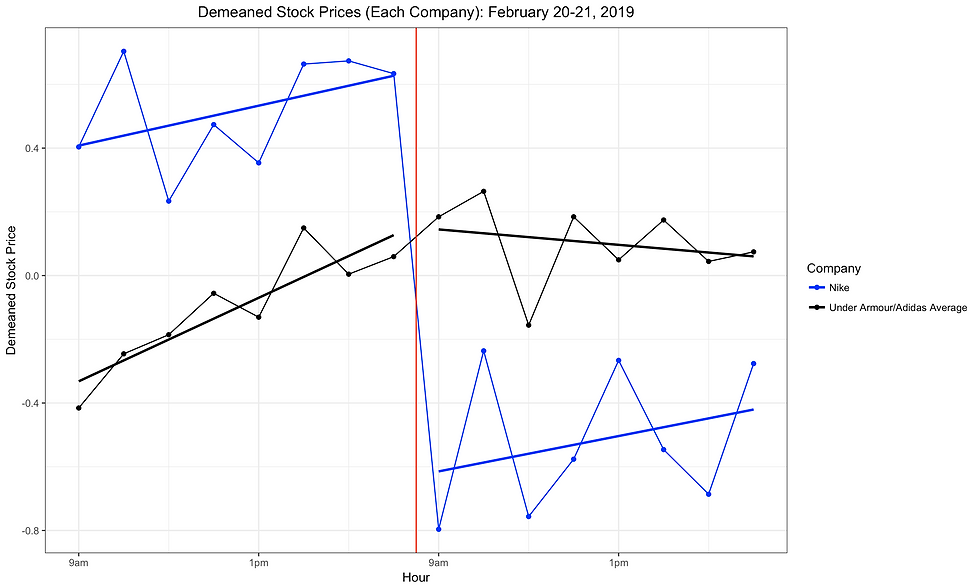

Your next logical concern should be: “looking at the graph above, it doesn’t look like the prices of Adidas or Under Armour are trending the same way as Nike before the explosion.” This is where the beauty of careful and rigorous econometrics comes in. We don’t need each “member” of the counterfactual group to be trending in the same direction as Nike, we just need the average of this group to be trending in the same direction. You can think of the average price of Under Armour and Adidas as it’s own company that now acts as a useful counterfactual for Nike, shown in the graph below:

Pretty similar trends in prices before the explosion (note: I use “demeaned” prices since the stock price levels are much different across the three companies). Now we can really see that Nike’s stock price (the blue line) drops significantly post-explosion, but not a whole lot happens to the price of the counterfactual group. This is the kind of rigor we need when examining and assessing causality.

These graphs are nice in telling us “yeah, looks like there’s some sort of impact.” But to really finish the job, we want to know how big that impact really is. Enter one of the favorite tools of applied econometricians: the linear regression. This is going to tell us “what is the exact magnitude of the impact of X on Y?” In this case, what is the effect of the explosion (X) on Nike’s stock price (Y)? What’s great about the regression is we can account (control) for what’s happening to prices in the counterfactual group, among other things (like general time trends in prices). Remember, we don’t just want to look at Nike’s price post-explosion vs. pre-explosion—we need to account for changes in the stock price of the counterfactual group (now the average of the Adidas and Under Armour stock prices) to make sure we’re getting the causal impact of the explosion on Nike’s price. The table below shows the results from a regression depicting the impact found in the previous figure:

Table: Effect of Zion Williamson Shoe Explosion on Stock Price

Let’s walk through this table. The dependent (Y) variable is the log of “Stock Price.” The independent (X) variable we care about is the “Post Explosion * Nike” variable. This represents the differential effect of the explosion on Nike’s stock price vs. the average of the counterfactual group’s stock prices. Since the dependent variable (Stock Price) is in log form, you can interpret this impact as a "1.6% decline in Nike’s stock price as a result of Zion’s explosion." The “stars” next to the estimate indicate that it is statistically significant, namely that we can be “confident” this effect exists. Just to be clear, the estimate on the “Post Explosion” variable (0.2%) represents the post-explosion impact on the non-Nike companies (e.g. Adidas and Under Armour), of which we can see there was no statistically significant impact at all (aka no stars). It is only the differential impact on Nike vs. the counterfactual group we care about – this removes any fallacy-based argument like the Colin Kaepernick one we discussed above. And so we’ve attained (plausible) causality!!

TLDR: it looks like the explosion did indeed immediately impact Nike’s stock price by an economically meaningful amount. While a 1.6% hit may not feel like a lot, it’s still significant money – Nike’s market cap was $133.52 billion on February 20th, which translates into a loss of $2.14 billion for the company. In terms of contextualizing this impact a bit further, it’s actually not a huge single-day dip percentage-wise. Over the past 5 years, the average percentage change in Nike’s day-to-day stock price was 0.07%, with a standard deviation of 1.5 percentage points. So, a 1.6% fall in Nike’s price from one day to the next is only slightly larger than a one standard deviation change from the average day-to-day price change over the past 5 years. This means this event isn’t a huge outlier (for additional context, the maximum day-to-day percentage change in Nike’s price over the past 5 years was 10.2% and the minimum was -10.1%). It’s also important to note that we’re measuring the immediate impact of the explosion on Nike’s price – this doesn’t provide evidence that this effect will persist in Nike’s stock price in the next several months or years. Depending on how competitors do or don’t take advantage of this event (we already saw Puma weigh in), or Nike’s response moving forward, the impacts may or may not last in the longer-term.

While the effect we’ve measured in this case is meaningful, the broader, more important takeaway is that it’s essential to think through the mechanism by which we measure these types of effects. It can be tempting (we see people do it all the time!) to just do a pre-post analysis on the group you think has been impacted. But without a reliable counterfactual, don’t even try and get causal with me.

(A modified/expanded version of this post was posted on Fansided: Nylon Calculus, which can be accessed here.)

Using technology to increase access to youth mental health support may offer a practical way for young people to reach guidance, safe-spaces, and early help without feeling overwhelmed by traditional systems. Digital platforms, helplines, and apps could give them a chance to seek support privately, connect with trained listeners-orexplore resources that might ease their emotional load. This gentle shift toward tech-based support may encourage youth to open-up at their own pace, especially when in-person help feels too heavy to approach.

There is always a chance that these tools-quietly make support feel closer than before, creating moments where help appears just a tap away. Even a small digital interaction might bring a sense of comfort. And somewhere in that space, you…

Detailed and practical, this guide explains concrete rebar in a way that feels approachable without oversimplifying. The step by step clarity is especially useful for readers new to the subject. I recently came across a construction related explanation on https://hurenberlin.com that offered a similar level of clarity, and this article fits right in with that quality. Great شيخ روحاني resource. explanation feels practical for everyday rauhane users. I checked recommended tools on https://www.eljnoub.com

s3udy

q8yat

elso9

This website demonstrates a structured approach to service information. Venue arrangements are described on sultan33, while reservation inquiries are managed via sultan33. The main homepage on sultan33 ties everything together.

This website demonstrates a structured approach to service information. Venue arrangements are described on sultan33, while reservation inquiries are managed via sultan33. The main homepage on sultan33 ties everything together.

This site offers a welcoming online experience, and I explored the main page through nixtoto to understand what’s available.